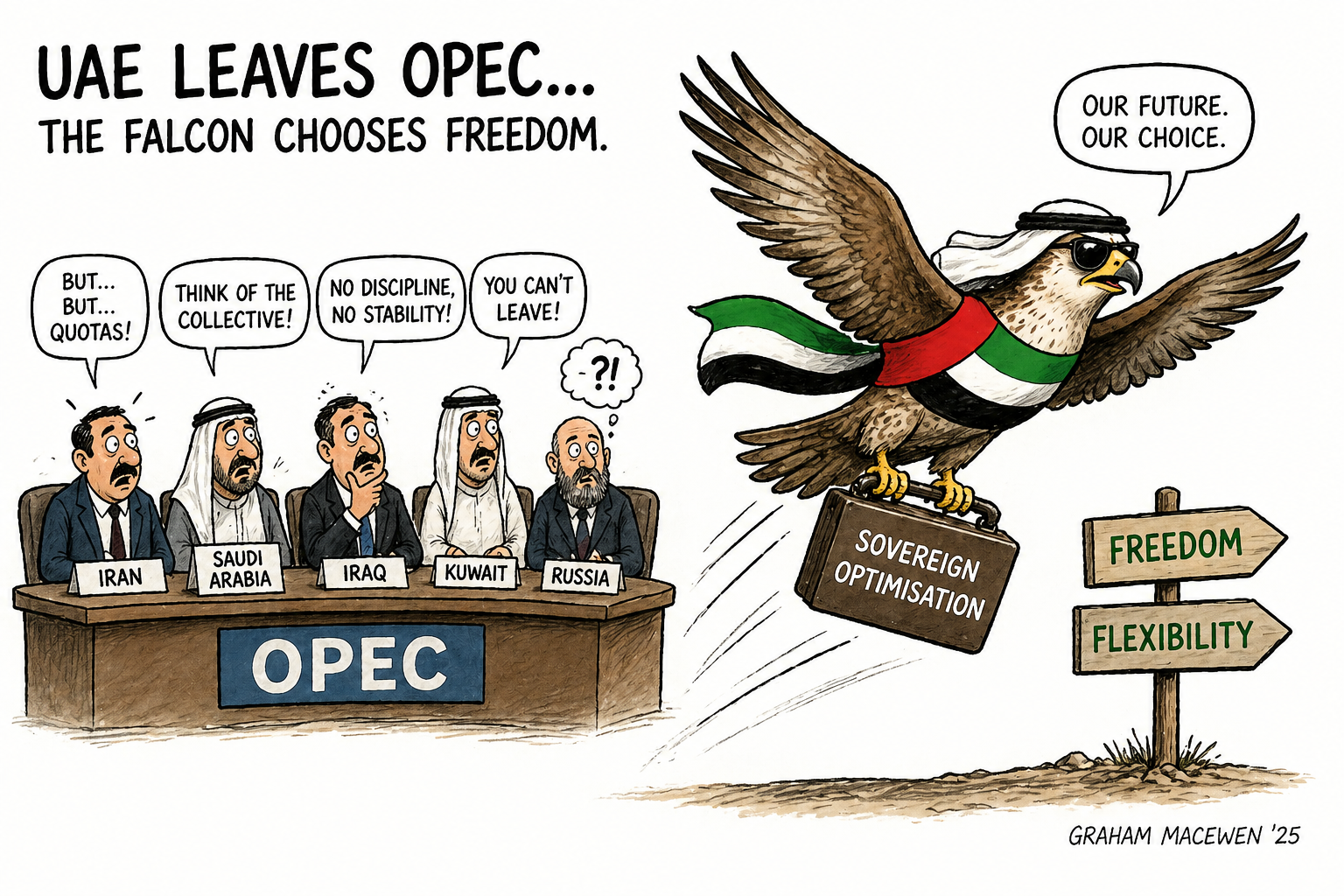

Wow! That was a tea-spluttering moment when I read the headlines this week – UAE to leave OPEC. I suppose a similar analogy would be a headline saying the UK to leave NATO (although after the Brexit fiasco I suspect that may yet happen!).

But should I have been so surprised?

I spent four very happy years in the UAE working for ADNOC (Abu Dhabi National Oil Company), and I remember having to get used to the fact that we could generally not talk about actual production numbers, but only production “capacity”. I also remember early on being staggered by the numbers involved. Take, for example, the Upper Zakum field. It started production in 1977 and, when I took up my position, it was producing around 750,000 bbls per day… and it was still increasing production after 45 years! I also remember the day it produced 1 million barrels in a single day for the first time. For context, when I left BP, its entire North Sea production was less than 150,000 barrels per day. And this was only one of ADNOC’s producing fields!

Our pride at the Upper Zakum million milestone was, of course, tempered by the fact that we were unlikely to be able to produce this quantity on an ongoing basis, as we were restricted by OPEC quotas and the organisation’s remit to manage market supply and, consequently, the oil price – a collective responsibility for their members’ benefit over the long term.

The UAE’s official reasons for leaving OPEC were a desire for production flexibility to align better with national energy strategy, and an ambition to capture market share through higher production.

However, it is the unspoken reasons that perhaps offer more insight and intrigue. I believe these are:

- a frustration with quotas and uneven compliance amongst members of OPEC (although, to be fair, there has been quite a lot of commentary that the UAE were as culpable of breaking quotas as any other member – I have no evidence to support this)

- an increasingly evident strategic rivalry with the Saudis – not just in terms of energy markets but also broader geopolitical issues

- the shock of the US/Israeli-led attack on Iran and the impact on the Strait of Hormuz

My take is that the UAE are leading (or perhaps just following) a trend from collective management to sovereign optimisation through a series of smaller alliances. For all Trump’s bluster and confusing government-by-social-media approach, his pronouncements on NATO, the UN, and WHO need to be taken seriously, and perhaps the UAE are seeing more value in stronger ties within an Israel/US/UAE axis than in the existing Gulf Cooperation Council and OPEC.

Let us also not forget that OPEC is now generally known as OPEC+, with the ex-officio participation of Russia, who have been associated with supporting Iran against Gulf interests. The Emiratis, who have borne the brunt of this and are known to be frustrated by the lack of assistance from their GCC neighbours, may well see greater security in the Abraham Accords approach than in traditional balancing acts (I suspect there are a great many Russian oligarchs and their yachts in Dubai feeling a tad nervous about this move!).

I also suspect that in the boardroom at ADNOC there will be a discussion on the reordering of priorities. If I were CEO of ADNOC (sadly I’m not – I fluffed the interview 😉), I would be sure to move investment in the Abu Dhabi Crude Oil Pipeline (ADCOP) to the top of the list. The pipeline was completed in 2011 and runs from the main Abu Dhabi oil-producing regions to the UAE’s Indian Ocean coast at Fujairah, bypassing the Strait of Hormuz.

The capacity of the pipeline is between 1.5 and 1.8 million barrels per day, which probably allows up to 50% of their oil exports to be shipped without relying on the Strait of Hormuz. With the UAE’s ambitious production expansion targets, this export route will become increasingly important. It’s all very well increasing production outside OPEC quotas, but you still have to access your markets.

Additionally, there is no telling how long hostilities with Iran could last, given the current leadership in Washington and Israel. Should things escalate, one option for Iran would be to call upon its proxies in Yemen to attempt to close the Bab al-Mandeb Strait, which would seriously constrain Saudi Arabia’s use of its own Hormuz-bypassing Petroline pipeline, which exports into the Red Sea.

I think the Emiratis’ bet is that flexibility is going to be more important than collective co-ordination in an uncertain future – both geopolitically and in terms of oil demand. The energy transition is uneven but, at the same time, inevitable, and so the race for the last barrels over the next few decades is likely to be fiercely fought.

So, for now, I think the OPEC cartel will endure, but perhaps the centre of gravity has shifted, and with it the balance between discipline and freedom in the global energy system.

My former colleagues have chosen to flex their falcon wings – good luck to them!

Leave a Reply